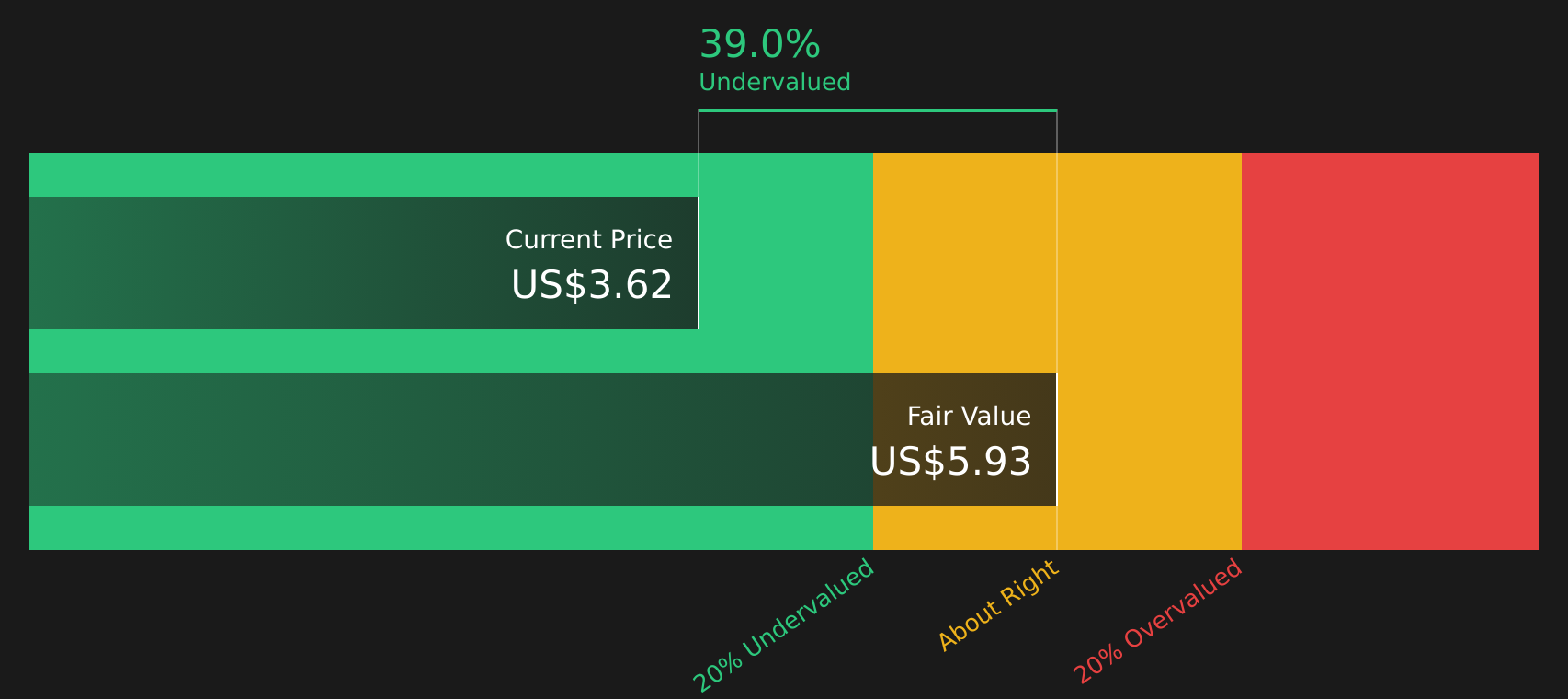

- This article examines whether Petco Health & Wellness Inc.’s current share price of $3.62 may represent a bargain or value trap based on the current share price of the business.

- The stock has experienced sharp moves recently, with returns of 52.1% over the past 7 days, 44.2% over the past 30 days, 27.0% year to date and 51.5% over the past year. However, the 3-year and 5-year returns show declines of 63.1% and 84.4%, which tell a very different story.

- These changes come as investors continue to re-evaluate the company after a long period of weakness. While there has been no headline event driving this particular move based on the data provided here, the difference between recent strength and a multi-year decline remains at the forefront of the mind for many shareholders.

- Simply put, Wall Street currently assigns Petco Health & Wellness a valuation score of 2 out of 6, which reflects how many of its checks suggest the stock is undervalued. We’ll then look at common methods of valuation and conclude with an approach to valuation that brings all the pieces together.

Petco Health & Wellness Inc. scores just 2/6 on our value checks. See what other red flags we found in the full value breakdown.

Method 1: Discounted Cash Flow (DCF) Analysis of Petco Health & Wellness Inc

The discounted cash flow, or DCF, model takes the cash flows expected to be generated in the future, then discounts those amounts back to what they might be worth in today’s dollars. It essentially asks what future cash flow is worth if you have it now.

For Petco Health & Wellness Inc., the model used is a 2-step free cash flow to equity approach based on cash flows available to shareholders. Trailing twelve month free cash flow is about $157.5 million. Analysts provide clear annual free cash flow forecasts through 2031, with estimates such as $191 million in 2031. Wall Street simply then extrapolates cash flows beyond the analyst’s horizon using a modest growth assumption.

After discounting these estimated cash flows today, the model comes to an estimated intrinsic value of about $5.93 per share. Compared to a recent share price of around $3.62, this DCF suggests the stock is trading at a roughly 39.0% discount. Only at this rate, the share price appears below the model’s intrinsic value estimate.

Conclusion: Undervalued

Our discounted cash flow (DCF) analysis suggests that Petco Health & Wellness Inc. is undervalued by 39.0%. Track it to your watchlist or portfolio, or discover 48 other high-quality stocks.

Go to the Company Valuation section of our report for more details on how we arrived at this fair value for Petco Health & Wellness Company.

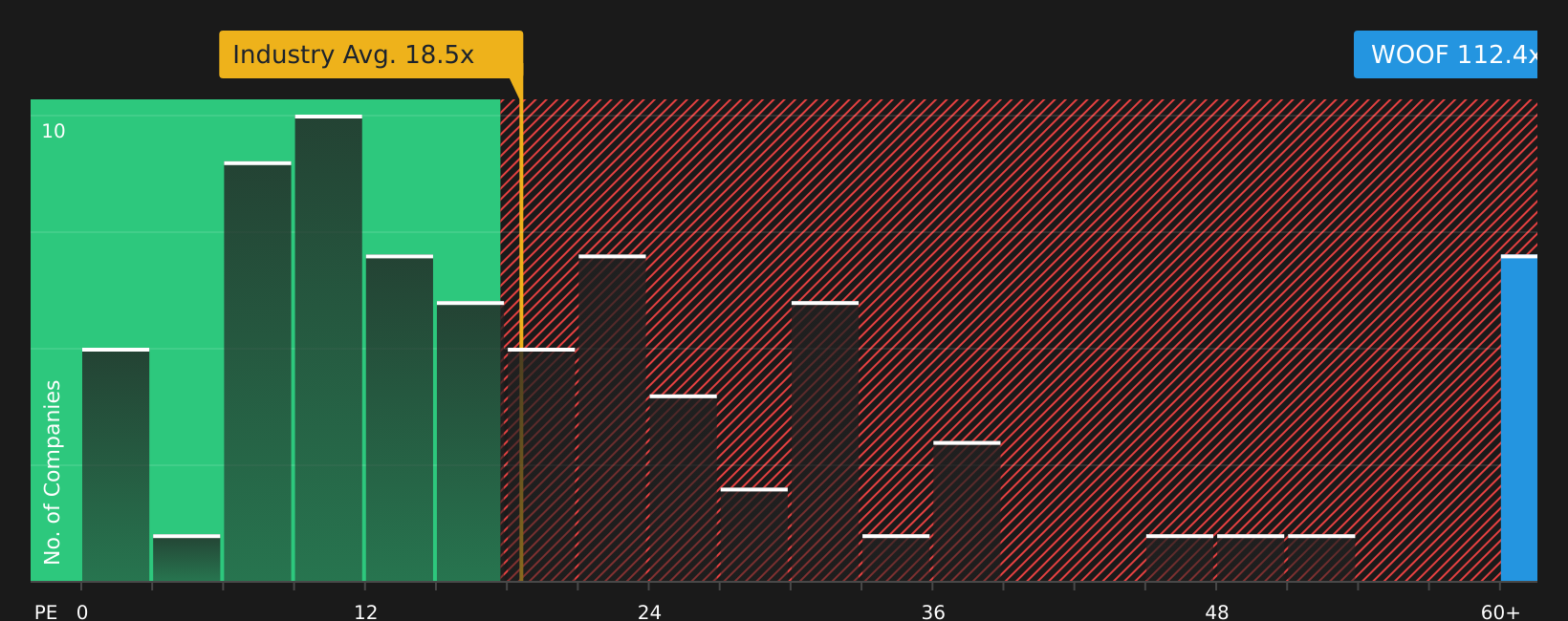

Method 2: Petco Health & Wellness Inc. Price vs. Earnings

For companies that generate earnings, the P/E ratio is a straightforward way to think about value, because it’s what you’re paying for each share relative to the profits that the business is currently generating.

In general, high growth expectations and low perceived risk can support a high P/E ratio, while slow growth and high risk usually justify a low multiple. So what counts as a “normal” or “fair” P/E varies across companies and industries.

Petco Health & Wellness Inc. trades at a P/E of about 112.40x, compared to the specialty retail industry average of about 18.49x and the peer average of about 17.72x. Simply put, Wall St. also calculates a “proper ratio” of 39.97x ownership. It represents the P/E ratio their model suggests appropriate factors such as earnings growth, industry, profit margin, market cap and risk profile.

This fair ratio can be more informative than a simple comparison to an industry or peer average, because it adjusts to Petco Health and Wellness Company’s unique characteristics and risk factors, rather than treating all retailers the same.

Compared to a current P/E of 112.40x with a reasonable ratio of 39.97x, the shares look expensive at this size.

The result: great value

The P/E ratio tells a story, but what if the real opportunity lies elsewhere? Start investing in legacy, not executive. Discover our top 19 founding companies.

Improve Your Decision Making: Choose Your Petco Health & Wellness Company Narrative

We mentioned earlier that there is an even better way to think about value, so let’s introduce you to narratives. Narratives allow you to connect a clear story to the numbers by connecting your idea of Petco Health & Wellness Company’s future revenue, earnings and margins and then to a fair value, all in one easy tool on a simple Wall St community page. This tool automatically updates when new news or earnings come in and helps you decide what to do by comparing your fair value to the current price, whether you lean toward a cautious view near the bearish fair value of US$2.72 or a more optimistic view near the US$5.14 bullish fair value.

For Petco Health & Wellness Inc., however, we’re going to make it really easy for you with a look at two leading Petco Health & Wellness Inc. statements:

The first is a very promising step that relies on animal welfare trends and the potential for better profits.

🐂 Bill Case of Petco Health and Wellness Company

Fair value in this bullish narrative: US$4.53 per share.

Current price vs. fair value: About 20.1% below this estimate, using simple Wall Street’s narrative fair value.

Annual income growth used in the model: 1.90%.

- Focus on integrating services like veterinary care and grooming with premium products, aiming for high customer lifetime value and strong margins in stores and digital.

- Emphasis on animal welfare, premium varieties and experiential retailing, with the view that this could support continued earnings growth if execution remains on track.

- Analysts in this camp work with earnings and margin assumptions that match the high end of current price targets, and they use a 12.5% discount rate to bring those expectations back to today.

Now there is a more cautious narrative that relies on execution risk, soft sales trends and pressure from online competition.

🐻 Petco Health & Wellness Company Bear Case

Fair value on this twelve-story: US$2.30 per share.

Current price vs. fair value: About 57.4% above this estimate, based on bearish narrative fair value.

Annual income growth used in the model: 0.61%.

- Highlighting ongoing pressure on net sales and comparable sales, with concerns that in-store traffic and e-commerce execution may limit future top-line growth.

- He cites tariff-related cost pressures, high debt and heavy capital investment as factors that could hamper flexibility if returns on these projects decline.

- It assumes a lower valuation multiple and uses less than 12% as a discount rate, reflecting a view that the market may be pricing in more success than these analysts believe.

Taken together, these narratives shape the current debate surrounding Petco Health and Welfare Inc., from a scenario where animal health and service growth supports a high fair value to where execution risks and soft sales argue for a low one. Your own view of store performance, e-commerce progress and future profitability will likely guide which side feels closest to how you view the stock today.

Curious about how the numbers become the stories that shape the markets? Explore community narratives

Do you think there is more to the story for Petco Health & Wellness Company? Join our community to see what others are saying!

This article by Simple Wall Saint is general in nature. We provide commentary based on historical data and analyst forecasts using only unbiased methodology and our articles are not intended to be financial advice. It does not recommend buying or selling any stocks, and does not take into account your goals, or your financial situation. We aim to bring you long-term focus analysis driven by fundamental data. Note that our analysis may not factor in recent price-sensitive company advertising or quality materials. Simply put, Wall St. has no position in the stock mentioned.

brand new: Manage your entire stock portfolio in one place

We have made The ultimate portfolio companion For stock investors, And it’s free.

• Connect to an unlimited number of portfolios and view your total in one currency

• Be alerted to new warning signs or hazards via email or mobile

• Track the fair value of your stocks

Try the demo portfolio for free

Have a comment about this article? Worried about content? Contact us directly. Alternatively, email editorial-team@simplywallst.com

#Time #Reconsider #Petco #Health #Wellness #WOOF #Share #Price #Rise